Backdoor and Mega Backdoor Roth: Should You or Shouldn't You?

For many savers the ROTH conversion and Mega ROTH conversion offer interesting opportunities. The details matter a lot.

John G T Slater, Jr

Managing Member

The standard Roth IRA contribution limit for 2026 is approximately $7,000 ($8,000 if you're 50 or older). The theoretical maximum you can funnel into Roth accounts using a Mega Backdoor Roth strategy exceeds $46,000 annually. That's a six-fold difference in tax-free growth capacity—and most high earners who could benefit from the larger strategy either don't know it exists or assume their 401(k) doesn't support it.

Both the Backdoor Roth IRA and the Mega Backdoor Roth are legitimate workarounds for income limits that otherwise lock high earners out of direct Roth contributions. But they operate through different mechanisms, carry different requirements, and fail spectacularly for different reasons. The Backdoor Roth trips up people with pre-tax IRA balances. The Mega Backdoor Roth is dead on arrival if your employer's plan lacks the right features.

This guide breaks down how each strategy works, who genuinely benefits, and—critically—who should stay away. These are powerful tools, but they're not universal solutions.

The Income Problem Both Strategies Solve

Direct Roth IRA contributions phase out entirely for single filers with modified adjusted gross income above approximately $165,000 and married couples filing jointly above $246,000 in 2026 (verify exact thresholds with the IRS or your CPA). If your income exceeds these limits, you cannot contribute directly to a Roth IRA regardless of how much you want the tax-free growth.

The appeal of Roth accounts is straightforward: qualified withdrawals in retirement are completely tax-free. No income tax on decades of compounded growth. No required minimum distributions during your lifetime (unlike Traditional IRAs and 401(k)s). For someone expecting to remain in a high tax bracket through retirement—or who values the certainty of knowing their future tax bill on those funds is zero—Roth accounts are compelling.

The Backdoor and Mega Backdoor strategies exist because while direct Roth contributions have income limits, certain conversions and rollovers do not. High earners can contribute through side doors that Congress left open.

How the Backdoor Roth IRA Works

The Backdoor Roth IRA is a two-step maneuver:

Step 1: Contribute to a Traditional IRA. There's no income limit preventing you from making a Traditional IRA contribution—only from deducting it. At high income levels, your contribution is non-deductible, meaning you get no tax benefit going in. You're contributing after-tax dollars.

Step 2: Convert the Traditional IRA to a Roth IRA. Conversions have no income limit. The converted amount is taxable, but if your Traditional IRA contains only non-deductible contributions and no earnings, your tax bill on conversion approaches zero.

The contribution limit for 2026 is approximately $7,000 ($8,000 for those 50 and older). This is modest compared to the Mega Backdoor, but it's accessible to anyone with earned income—no employer plan required.

The Pro-Rata Rule: Where Backdoor Roth Conversions Go Wrong

Here's the trap: the IRS doesn't let you cherry-pick which dollars you convert. If you have any pre-tax money in any Traditional, SEP, or SIMPLE IRA, the pro-rata rule requires you to treat each dollar converted as a proportional mix of pre-tax and after-tax funds.

Example: Sarah has a $93,000 rollover IRA from a former employer (all pre-tax). She makes a $7,000 non-deductible Traditional IRA contribution and immediately converts it, expecting zero tax because she just put in after-tax money.

The IRS disagrees. Her total Traditional IRA balance across all accounts is $100,000. Of that, $7,000 (7%) is after-tax, and $93,000 (93%) is pre-tax. When she converts $7,000, the IRS treats 93% of it—$6,510—as taxable income. Only $490 of her conversion is tax-free.

If Sarah is in the 35% bracket, she owes approximately $2,279 in federal tax on what she thought was a slick tax-free maneuver. The strategy didn't fail because of an error in execution; it failed because she had pre-tax IRA balances.

The aggregation is merciless. It includes rollover IRAs, SEP IRAs, SIMPLE IRAs, and any Traditional IRA you hold anywhere. The only way to make Backdoor Roth work cleanly is to have zero pre-tax IRA balances on December 31st of the conversion year.

The Reverse Rollover Fix

If you have pre-tax IRA money but still want to execute a Backdoor Roth, there's a potential solution: roll those pre-tax IRA funds into your current employer's 401(k) before converting. Employer plan balances don't count in the pro-rata calculation—only IRA balances do.

This only works if your 401(k) accepts incoming rollovers, and not all plans do. Check with your plan administrator before assuming this path is open.

How the Mega Backdoor Roth Works

The Mega Backdoor Roth operates through your employer's 401(k) or 403(b) rather than through IRAs. It allows dramatically larger annual contributions to Roth accounts—potentially $46,000 or more beyond your regular 401(k) deferrals.

The mechanics involve three distinct contribution buckets in a 401(k):

1. Employee pre-tax or Roth deferrals: Capped at approximately $23,500 for 2026 ($31,000 with standard catch-up for ages 50+, or potentially higher with the SECURE 2.0 super catch-up for ages 60-63—verify current rules with your HR department).

2. Employer contributions: Matching contributions, profit sharing, etc.

3. Employee after-tax contributions: This is the bucket that enables Mega Backdoor Roth. After-tax contributions are not tax-deductible and are separate from your regular deferrals.

The total of all three categories cannot exceed the 415(c) limit—approximately $70,000-$71,000 for 2026 (verify exact figure). If you're maximizing your employee deferrals at $23,500 and your employer contributes $10,000 in matching, you could potentially make after-tax contributions of roughly $36,500-$37,500 to reach the 415(c) ceiling.

The conversion step: Once you've made after-tax contributions, you convert or roll them into a Roth account. This can happen two ways:

- In-plan Roth conversion: Your after-tax 401(k) money converts to designated Roth 401(k) money within the same plan.

- In-service withdrawal to Roth IRA: You roll the after-tax contributions out of the 401(k) and into your personal Roth IRA while still employed.

The first approach keeps money in the 401(k) (which may have better creditor protection). The second gives you more investment options and separates the funds from your employer. Both accomplish the goal of getting after-tax contributions into Roth status.

The Two Plan Features You Must Verify

The Mega Backdoor Roth is impossible unless your employer's plan has both of the following:

1. After-tax contributions allowed. Many 401(k) plans don't offer this option at all. It's separate from Roth 401(k) deferrals—after-tax contributions are a distinct category that not all plans support.

2. In-plan Roth conversions OR in-service withdrawals of after-tax contributions. Making after-tax contributions is only half the equation. You need a mechanism to move those funds into Roth status. If your plan allows after-tax contributions but doesn't permit either conversion or in-service withdrawal, the money sits in after-tax limbo—growing tax-deferred, with gains eventually taxable as ordinary income upon distribution.

Contact your HR department or plan administrator directly. Ask: "Does our plan allow employee after-tax contributions? And if so, can I do in-plan Roth conversions or take in-service withdrawals of those contributions?" If the answer to either question is no, the Mega Backdoor Roth isn't available to you through that employer.

Who Should Pursue These Strategies

High earners above Roth phase-out thresholds with significant savings capacity. If your household income puts you above direct Roth contribution limits and you're already maximizing tax-deferred space (401(k), HSA), these strategies let you add more to tax-free accounts. The Mega Backdoor is particularly valuable for families with six-figure incomes who can save aggressively.

Investors expecting to remain in high tax brackets through retirement. Roth accounts shine when you expect future tax rates (personal or legislative) to be as high or higher than today's. If you're a 55-year-old executive planning to retire at 62 with pension income, Social Security, and required minimum distributions pushing you into the 32%+ bracket, tax-free Roth withdrawals become increasingly attractive.

Those seeking tax diversification. Even if you're uncertain about future rates, having a mix of pre-tax (Traditional 401(k)/IRA), after-tax (taxable brokerage), and Roth accounts gives flexibility. You can manage taxable income in retirement by choosing which bucket to draw from each year.

People with long time horizons. Tax-free compounding needs time to generate meaningful benefits. A $46,000 Mega Backdoor contribution at age 45 growing at 7% annually becomes approximately $180,000 by age 65—all withdrawable tax-free. The same contribution at 63 has only two years to grow before typical retirement.

Clean IRA situations (for Backdoor Roth specifically). If you have no pre-tax IRA balances—perhaps because you've always kept retirement savings in employer plans—the Backdoor Roth executes cleanly. The pro-rata rule is irrelevant when there's nothing to aggregate.

## Who Should Not Pursue These Strategies

Holders of substantial pre-tax IRA balances (for Backdoor Roth). If you have $200,000 in a rollover IRA from previous employers and no current 401(k) that accepts rollovers, the Backdoor Roth will be almost entirely taxable. The strategy doesn't work. You'd be paying ordinary income tax to convert funds that started as after-tax dollars—the opposite of tax efficiency.

Employees without qualifying plan features (for Mega Backdoor). No amount of desire or careful planning overcomes a plan that simply doesn't allow after-tax contributions or in-service conversions. This isn't a matter of execution; it's a plan design limitation. If your employer's plan doesn't support it, you cannot do it.

Low-income years when direct Roth contributions are available. If your income temporarily dips below Roth phase-out thresholds—sabbatical, career transition, starting a business—skip the backdoor complexity. Contribute directly to a Roth IRA. Simpler execution, same result.

Those with near-term liquidity needs. Roth IRA contributions (not earnings) can be withdrawn penalty-free at any time. But if you're funding a Mega Backdoor Roth while simultaneously struggling to maintain a six-month emergency fund, the prioritization is questionable. Tax optimization matters less than not running out of money.

People retiring soon into a lower tax bracket. If you're 64, planning to retire at 66, and expect your income to drop from the 32% bracket to the 12% bracket, the Roth advantage diminishes. You'd be paying 32% now for tax-free withdrawals you could otherwise take at 12%. The math may not favor conversion.

Execution Checklist: Doing This Correctly

For a Backdoor Roth IRA:

1. Confirm you have zero pre-tax Traditional, SEP, or SIMPLE IRA balances. If not, explore rolling them into your 401(k) first.

2. Open a Traditional IRA if you don't have one. Make a non-deductible contribution (the 2026 limit, approximately $7,000 or $8,000 if 50+).

3. Wait for the contribution to settle (typically 1-3 business days). Waiting longer increases the earnings subject to tax upon conversion, though the amounts are usually trivial.

4. Convert the entire Traditional IRA balance to a Roth IRA. This is a separate transaction from the contribution.

5. File Form 8606 with your tax return. Part I reports your non-deductible contribution. Part II reports the conversion. This form is how the IRS knows not to tax the basis you already contributed after-tax.

For a Mega Backdoor Roth:

1. Verify your plan allows after-tax contributions and in-plan Roth conversions (or in-service withdrawals to a Roth IRA). Get this in writing from HR or your plan administrator.

2. Calculate your available after-tax contribution room: 415(c) limit minus employee deferrals minus employer contributions.

3. Elect after-tax contributions through your payroll system. This is typically a separate election from your pre-tax or Roth 401(k) deferral.

4. Execute conversions promptly after each contribution. Some plans allow automatic same-day conversion, which minimizes taxable earnings. If your plan requires manual conversions, do them monthly or quarterly.

5. Track your basis carefully. If you roll over to a Roth IRA, ensure your custodian receives proper documentation of the after-tax amount versus any earnings.

SECURE 2.0 Consideration: Mandatory Roth Catch-Up

Beginning in 2024 (with some transition relief into 2025), SECURE 2.0 required that catch-up contributions for employees earning over $145,000 in FICA wages be made as Roth deferrals rather than pre-tax. This doesn't change Mega Backdoor Roth mechanics directly, but it does mean high earners making catch-up contributions are already adding to Roth 401(k) balances regardless of preference. Verify the current status and your plan's implementation with your HR department, as some provisions faced administrative delays.

The Decision Framework

Consider the Backdoor Roth IRA if:

- Your income exceeds Roth phase-out limits

- You have zero pre-tax IRA balances (or can roll them into a 401(k))

- You want steady annual Roth contributions without employer plan dependence

Consider the Mega Backdoor Roth if:

- You're already maximizing standard 401(k) deferrals

- Your employer plan supports after-tax contributions and conversions

- You have substantial additional savings capacity beyond standard retirement limits

- You want to accelerate tax-free wealth accumulation

Skip both strategies if:

- Pre-tax IRA balances make Backdoor conversions punitive

- Your employer plan lacks required features

- You're in a low-income year where direct Roth contributions are simpler

- You're retiring soon into a significantly lower tax bracket

These aren't set-it-and-forget-it decisions. Plan features change, income fluctuates, and tax laws evolve. Revisit annually with your financial advisor and CPA to confirm the strategies still align with your situation.

---

This article is provided for educational purposes by CUBIC Advisors LLC, a registered investment adviser with the Commonwealth of Pennsylvania (CRD #165008). The information presented is not personalized investment, tax, or legal advice. Individual circumstances vary significantly; consult with qualified professionals—including your CPA, attorney, and financial advisor—before implementing any strategy discussed. Tax laws and retirement plan rules are subject to change. Past approaches do not guarantee future applicability.

To discuss whether these strategies fit your specific financial situation, contact CUBIC Advisors for a complimentary consultation.

---

Tags

Related Articles

HSA as a Retirement Account: The Triple-Tax-Advantage

Why a properly invested HSA can outperform a 401(k) per dollar of contribution.

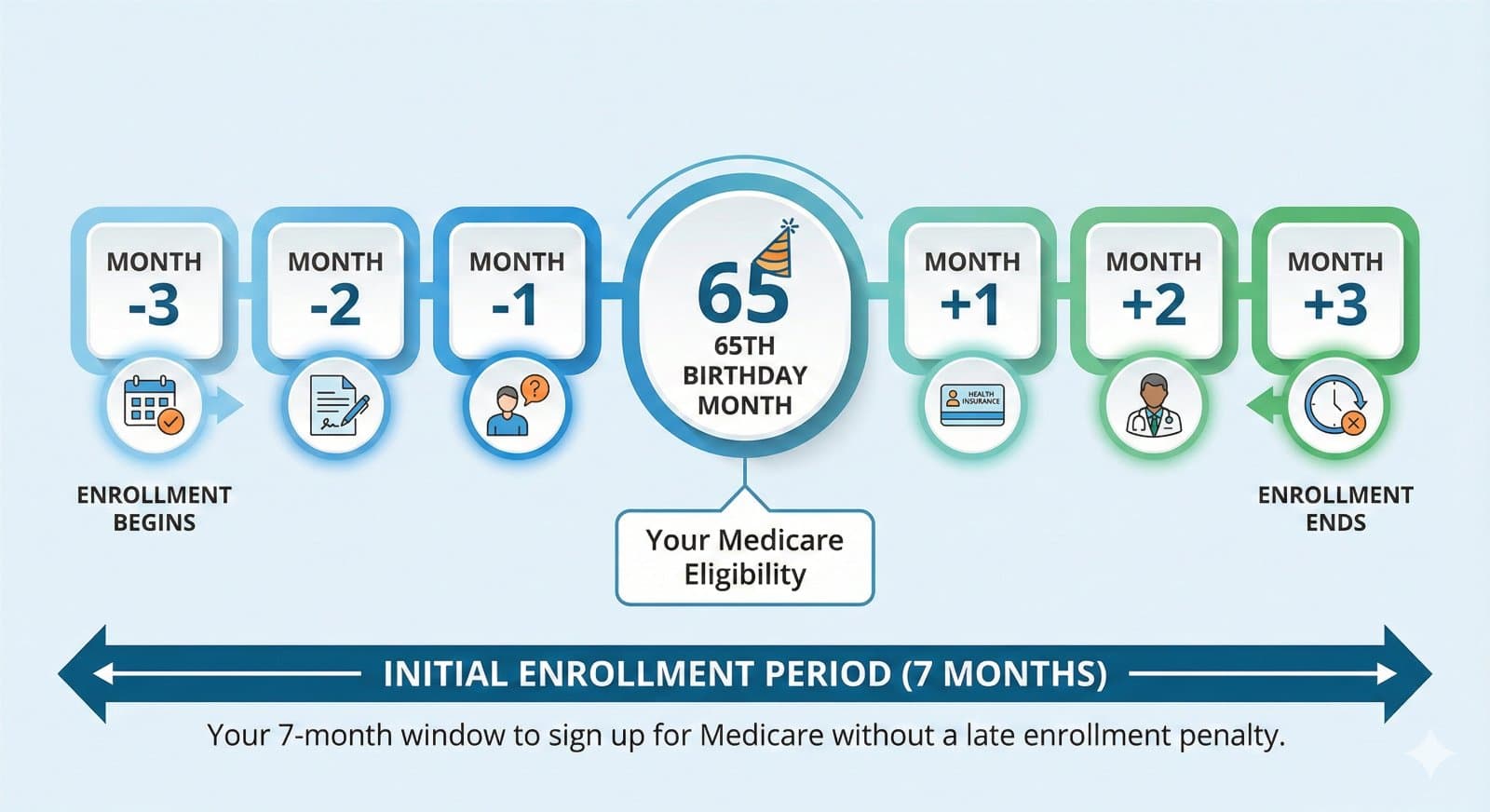

The Medicare Deadline Nobody Tells You About: What to Do Before You Turn 65

Turning 65 triggers a critical seven-month enrollment window for Medicare, and missing it can result in lifetime penalties of approximately 10% per year on your Part B premium. The 2025 Inflation Reduction Act caps prescription drug costs at $2,000 annually and eliminates the coverage gap, making timely enrollment more valuable than ever.

Disclaimer: CUBIC Advisors and its clients may hold positions in, and may trade, securities of companies discussed in these blog posts. The information provided is for educational and informational purposes only and should not be construed as financial, investment, retirement, tax, or legal advice. Readers should consult with their own qualified advisors before making any financial decisions. Past performance does not guarantee future results.