HSA as a Retirement Account: The Triple-Tax-Advantage

Why a properly invested HSA can outperform a 401(k) per dollar of contribution.

John G T Slater, Jr

Managing Member

HSA as a Retirement Account: The Triple-Tax-Advantage Playbook (2026)

The average American over 65 holds roughly $9,000 in their Health Savings Account, per Employee Benefit Research Institute data. Fidelity estimates that a 65-year-old couple retiring in 2025 will spend approximately $345,000 on healthcare costs over the rest of their lives, excluding long-term care. That gap, between what people have set aside and what they will actually need, represents one of the more glaring missed opportunities in personal finance.

The HSA is the only account in the Internal Revenue Code that offers a true triple-tax advantage. Contributions reduce taxable income, growth compounds tax-free, and withdrawals for qualified medical expenses escape taxation entirely. Dollar for dollar, a properly managed HSA can outperform a 401(k) as a wealth-building vehicle. Yet most account holders treat it as a glorified checking account for copays, leaving the cash uninvested and forfeiting decades of tax-free compounding.

For affluent individuals approaching or in retirement, the HSA deserves to be treated as a core position, not an afterthought.

The Triple-Tax Advantage Explained

Three distinct tax benefits stack inside an HSA in ways unavailable elsewhere in the tax code.

Benefit one: deductible contributions. HSA contributions reduce your federal adjusted gross income dollar for dollar. Unlike traditional IRA deductions, which phase out at higher income levels, HSA deductions carry no income ceiling. A surgeon earning $900,000 and a teacher earning $65,000 capture the full deduction if they are otherwise eligible.

Benefit two: tax-free growth. Once inside the HSA, dividends, interest, and capital gains accumulate without triggering current taxation. This is similar to a Roth, with one important distinction we will address shortly.

Benefit three: tax-free withdrawals for qualified medical expenses. When you withdraw funds for IRS-approved healthcare costs (prescriptions, dental and vision care, Medicare premiums, long-term care insurance, and many others), no federal tax applies. The money went in untaxed, grew untaxed, and comes out untaxed.

Compare this to your other retirement vehicles:

Traditional 401(k) and IRA: deductible going in, tax-deferred growth, fully taxed on withdrawal.

Roth 401(k) and IRA: after-tax contributions, tax-free growth, tax-free withdrawal.

HSA used for qualified medical: deductible going in, tax-free growth, tax-free withdrawal.

A Roth offers two of three benefits. A traditional account offers one and a half (the tax-deferred growth still faces eventual taxation on withdrawal). Only the HSA delivers all three when used for qualifying expenses. That mathematical superiority explains why thoughtful planners increasingly view the HSA as their first priority within the retirement savings hierarchy, not their last.

2026 Contribution Limits and Eligibility

The IRS published the 2026 inflation adjustments in Revenue Procedure 2025-19. To contribute to an HSA you must be enrolled in a High-Deductible Health Plan, must not be covered by other disqualifying health coverage, must not be enrolled in Medicare, and must not be claimed as a dependent on someone else's return.

For 2026, the contribution limits are:

Self-only coverage: $4,400

Family coverage: $8,750

Age 55+ catch-up contribution: an additional $1,000

To qualify as an HDHP in 2026, your plan must meet minimum deductibles and stay below maximum out-of-pocket caps:

Self-only: minimum deductible $1,700, maximum out-of-pocket $8,500

Family: minimum deductible $3,400, maximum out-of-pocket $17,000

One frequently overlooked detail involves spousal contributions. If you carry family HDHP coverage, you contribute up to the family limit regardless of whether your spouse has separate coverage. However, if both spouses are 55 or older, each must open their own HSA to claim their respective $1,000 catch-up contribution. The catch-up cannot be doubled into a single account.

Contributions for a tax year may be made up until that year's tax filing deadline, typically April 15 of the following year. This gives you a planning window after year-end to optimize the prior year's tax position.

The Shoebox Method: Maximizing Long-Term Growth

The conventional way to use an HSA is as a medical-spending account. Incur expense, submit claim, receive reimbursement. That approach captures the tax benefits, but it sacrifices decades of tax-free compounding.

The shoebox method inverts this logic:

Pay qualifying medical expenses out of pocket from taxable funds.

Save every receipt with date, provider, and amount documented.

Let the HSA balance grow untouched for years or decades.

Reimburse yourself tax-free at any point in the future.

The IRS places no deadline on when you can reimburse yourself for qualifying expenses incurred after your HSA was established. A $500 prescription filled in 2026 can be reimbursed tax-free in 2046, and the HSA balance compounds uninterrupted for those twenty years.

Consider the math. You incur $4,000 in annual medical expenses and have two options.

Option A — immediate reimbursement. You withdraw $4,000 from your HSA each year. The balance never compounds because you are spending as fast as you contribute.

Option B — shoebox method. You pay the $4,000 from a taxable brokerage account and let the HSA grow. Twenty years later, your accumulated receipts represent $80,000 in tax-free reimbursement potential, and your HSA has compounded without interruption. Assuming 7% growth, the $4,000 you would have withdrawn in year one is worth roughly $15,500 by year twenty.

Implementing this strategy requires discipline and documentation. Digital receipt storage through dedicated apps or simple cloud folders ensures you will not lose proof of expenses years later. Several HSA platforms offer receipt-saving features designed specifically for the shoebox approach.

Investing Your HSA: Beyond the Cash Default

Most HSA custodians default new accounts to a cash-savings option yielding somewhere between negligible and insulting. Unless you actively opt into the investment menu, your contributions sit in what amounts to a low-yield money-market position.

This is the single most common HSA mistake among otherwise sophisticated investors. The same people who carefully allocate their 401(k) across diversified equity and fixed-income positions leave their HSA languishing in cash for years.

Custodians typically require you to maintain a cash threshold (often $1,000 to $2,000) before accessing investment options. Once you clear that floor, the remainder can go into mutual funds, ETFs, or other securities depending on the platform.

Investment selection inside an HSA follows the same principles as any long-term account. For someone with a 15-plus year horizon before anticipated withdrawals, equity-heavy allocations capture growth potential without current tax drag. Because no capital gains tax applies inside the wrapper, you can rebalance freely without triggering taxable events.

Not all HSA providers are created equal. Key differentiators:

Fee structure. Some providers charge monthly administrative fees, per-trade commissions, or elevated expense ratios on available funds. Others have eliminated most fees to compete for assets.

Investment menu quality. Certain custodians limit you to a short list of proprietary or revenue-sharing funds. Better platforms offer broad access to low-cost index funds or individual securities.

Cash threshold requirements. Lower thresholds mean more of your balance is invested rather than parked.

Integration and usability. Whether the platform integrates with your other accounts and provides reasonable tools for tracking and documentation.

Fidelity's HSA has earned recognition for charging no administrative fees, requiring no minimum investment threshold, and offering access to the firm's full investment lineup. Lively and HSA Bank are also widely used and offer competitive structures. If your employer's HSA has poor terms, you can transfer accumulated balances to a custodian of your choice while keeping the employer-payroll account active for new contributions.

A Note for Pennsylvania Residents

Pennsylvania conforms cleanly to federal HSA treatment for ordinary use, which is not true of every state. Per the PA Department of Revenue, HSA contributions deductible under IRC § 223 for federal purposes may be claimed as a deduction on the PA personal income tax return (on PA Schedule O for direct contributions; W-2 Box 12 code W contributions are already excluded from PA wages). Qualified-medical distributions are not subject to PA personal income tax. And — importantly — Pennsylvania does not tax interest, dividends, or capital gains accruing inside the HSA. Only California and New Jersey treat HSAs as fully taxable accounts at the state level; Pennsylvania does not.

The principal state-level differences worth knowing: non-qualified distributions are taxable in PA as interest income on PA-40 Schedule A, but PA does not incorporate the 20% federal penalty under IRC § 223(f)(4) (the federal 20% still applies separately). Excess employer contributions are subject to PA tax as compensation. State rules can change; confirm current treatment with a CPA who handles PA returns.

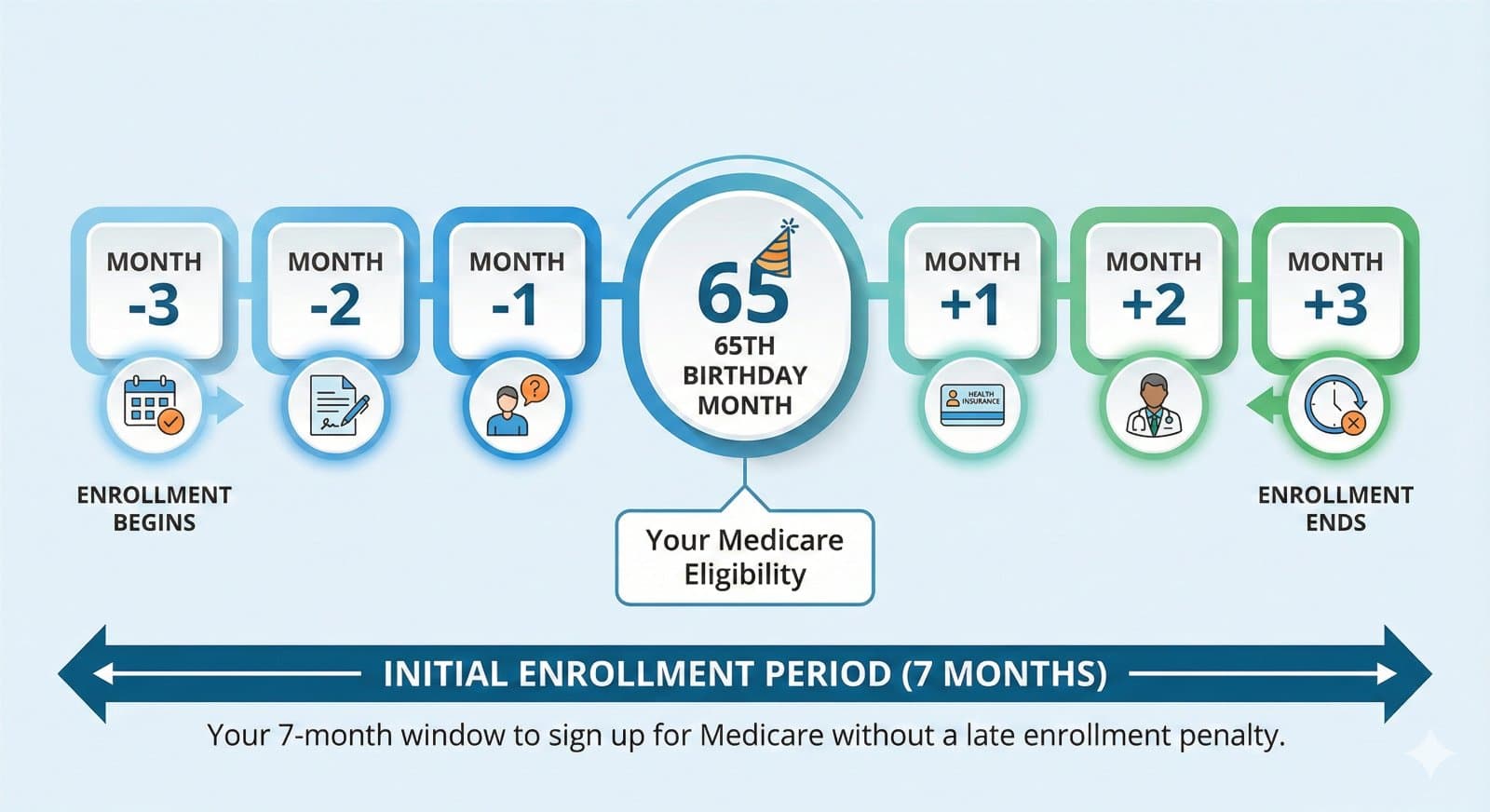

The Medicare Cliff

At age 65, or whenever you enroll in any Medicare coverage (Part A, B, or D), your HSA contribution eligibility ends. This catches many people by surprise.

Even if you continue working with employer coverage past 65, enrolling in Medicare Part A (which happens automatically for those who have begun Social Security) terminates HSA contribution eligibility. People who delay Social Security past 65 can continue HSA contributions if they remain on qualifying employer coverage and decline Medicare enrollment.

One sharp edge to be aware of: when you do eventually enroll in Medicare after age 65, Part A coverage is back-dated up to six months (or to your 65th birthday, whichever is later). HSA contributions made during that retroactive window become excess contributions subject to a 6% annual excise tax until withdrawn. People planning to enroll in Medicare should stop HSA contributions at least six months prior.

This creates several planning considerations.

Maximize contributions before the cliff. A 60-year-old on family HDHP coverage has roughly five years of contribution runway remaining. At 2026 limits, a couple where both spouses are 55+ could add approximately $53,750 to their HSAs over those five years (the family limit of $8,750 plus $2,000 in combined catch-up contributions, annually for five years), before any growth.

You can still use the HSA after 65. Contribution eligibility ends, but withdrawals continue functioning normally. Qualified medical expenses remain tax-free, and the list of qualified expenses includes most Medicare premiums (Parts B, C, and D, though not Medigap), long-term care insurance premiums (within IRS-specified limits), and out-of-pocket costs.

Non-medical withdrawals change character at 65. Before age 65, non-medical HSA withdrawals trigger ordinary income tax plus a 20% penalty. After 65, the penalty disappears. Non-medical withdrawals become taxable as ordinary income but carry no additional penalty. The HSA effectively converts to a traditional IRA for non-medical purposes once you cross that age threshold. Given the trajectory of healthcare costs in retirement, the tax-free medical pathway typically remains the more valuable use.

A 30-Year Worked Example

Consider a 35-year-old professional beginning consistent HSA contributions with plans to retire at 65. Assume family HDHP coverage throughout, contributions at the family limit each year, the $1,000 catch-up beginning at age 55, and 7% average annual growth.

For simplicity, hold the contribution dollar amounts at 2026 levels (in reality the limits index up over time, which strengthens the HSA case relative to the math below):

Years 1-20 (ages 35-54): $8,750 annual contribution

Years 21-30 (ages 55-64): $9,750 annual contribution (adding the $1,000 age-55 catch-up)

Total contributions: $272,500

Ending balance at 7% growth: approximately $870,000 (assuming monthly payroll-funded contributions; end-of-year lump-sum contributions produce ~$840,000)

At age 65, this individual has roughly $870,000 available for tax-free medical reimbursement, plus the documented decades of receipts under the shoebox method to draw against tax-free at any point.

Compare to the same dollars contributed to a taxable brokerage account by someone in the 24% federal bracket. The contribution dollars themselves cost more (roughly $65,000 in additional federal tax over 30 years, since they are not deductible), and the taxable account suffers an annual tax drag of 1-1.5% on dividends and realized gains. Final balance at an effective after-tax growth rate of around 5.5-6%: roughly $680,000 to $750,000.

The HSA advantage in this comparison is approximately $120,000 to $190,000 in additional ending wealth, plus the taxes saved on contributions, plus avoidance of capital-gains tax on appreciation when funds are withdrawn for qualified medical expenses.

The numbers shift if your future medical needs are very low (in which case non-medical withdrawals after 65 still face ordinary income tax) or very high (in which case the HSA wins by even more).

Common Mistakes

Leaving balances in cash. Every dollar parked in a money-market option forfeits tax-free compounding. Establish your cash floor and invest the rest according to your time horizon.

Inadequate receipt documentation. The shoebox method only works if you can substantiate expenses years or decades later. Develop a systematic approach to capturing receipts digitally with date, provider, and amount.

Contributing after Medicare enrollment. Excess contributions trigger a 6% annual penalty until corrected. The moment you enroll in any Medicare coverage, stop HSA contributions, and remember that Medicare Part A back-dates up to six months when you enroll past 65.

Ignoring the spouse opportunity. Married couples on family HDHP coverage can contribute the full family limit. If both spouses are 55+, each needs their own HSA to capture the full $1,000 catch-up.

Failing to consolidate or transfer. Employer HSAs often have weaker investment options or higher fees than standalone custodians. Transfer accumulated balances to a better platform while keeping the employer account active for new payroll deposits.

Overlooking inheritance treatment. A surviving spouse inherits an HSA as their own HSA, with no immediate tax. A non-spouse beneficiary, on the other hand, faces the entire account balance taxed as ordinary income in the year of the original owner's death (though the beneficiary can reduce that taxable amount by paying the decedent's qualified medical expenses within one year of death). For estates where non-spouse beneficiaries are likely, this materially changes the case for spending HSA balances down on qualifying expenses during your lifetime.

Where the HSA Fits in a Broader Strategy

The HSA performs best when it is coordinated with your other accounts, not managed in isolation. A reasonable contribution priority for most high-income earners:

Capture the full employer 401(k) match (free money before anything else).

Maximize HSA contributions.

Maximize remaining 401(k) or 403(b) space.

Fund a Backdoor Roth IRA if income exceeds direct Roth limits.

Taxable investment accounts.

This sequence prioritizes the triple-tax advantage first, then the dual-tax advantage of Roth vehicles, then single-benefit traditional accounts. In retirement, the order matters in reverse: drawing from an HSA for early-retirement medical spending preserves traditional account balances for required minimum distributions and preserves Roth balances for tax-free legacy planning.

The HSA is not a silver bullet. It requires HDHP enrollment, which is not appropriate for every health situation. It carries administrative complexity and demands disciplined documentation. But for eligible individuals with long time horizons, it is one of the more mathematically advantageous accounts available.

Taking Action

Confirm your current health plan's HDHP eligibility. If you maintain an employer HSA, evaluate its fee structure and investment options against standalone custodians and consider whether to transfer accumulated balances. Establish a digital documentation system before you start spending out of pocket on the shoebox method. Coordinate timing of contributions with your CPA, particularly around year-end.

If you would like to discuss how HSA optimization fits within your broader retirement plan, contact CUBIC Advisors for a complimentary consultation.

This article is provided for educational purposes by CUBIC Advisors, LLC, a registered investment adviser with the Commonwealth of Pennsylvania (CRD #165008). The information presented is not personalized investment, tax, or legal advice. HSA rules involve complex eligibility requirements and tax consequences that vary based on individual circumstances, including state of residence; consult your CPA or tax attorney regarding your specific situation. Registration as an investment adviser does not imply a particular level of skill or training. Past results are not indicative of future outcomes.

Tags

Related Articles

Backdoor and Mega Backdoor Roth: Should You or Shouldn't You?

For many savers the ROTH conversion and Mega ROTH conversion offer interesting opportunities. The details matter a lot.

The Medicare Deadline Nobody Tells You About: What to Do Before You Turn 65

Turning 65 triggers a critical seven-month enrollment window for Medicare, and missing it can result in lifetime penalties of approximately 10% per year on your Part B premium. The 2025 Inflation Reduction Act caps prescription drug costs at $2,000 annually and eliminates the coverage gap, making timely enrollment more valuable than ever.

Disclaimer: CUBIC Advisors and its clients may hold positions in, and may trade, securities of companies discussed in these blog posts. The information provided is for educational and informational purposes only and should not be construed as financial, investment, retirement, tax, or legal advice. Readers should consult with their own qualified advisors before making any financial decisions. Past performance does not guarantee future results.